For the major averages as the soft or survey and opinion data continues to scream recession. While the hard or factual data and the incoming earnings data has another huge week. Since Monday the S&P 500 gained 162 points or 2.93%, the NASDAQ is up 595 points or 3.42% while the DOW jumped 1,204 points or 3%. So much for all the chicken littles over at the mainstream media hollering about the Trump administration destroying everything in sight.

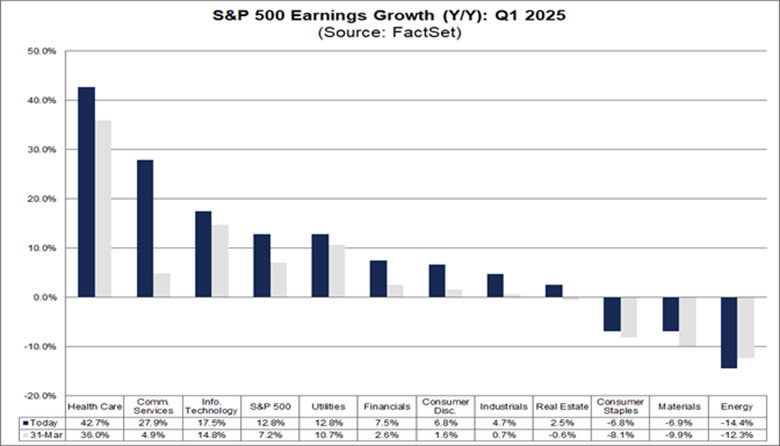

The latest show me the money update from FactSet Research shows another huge week for S&P 500 earnings growth as Q-1 earnings growth jumped from +10.1% to + 12.8% putting it on track for a second consecutive quarter of double digit earnings growth. Revenue growth is running a healthy 4.8% a little over 60% of companies have reported so far. Thanks to FactSet for the chart.

A Busy Economic Calendar

Q-1 preliminary GDP hit the tape Wednesday with estimates all over the map from the deeply negative -2.5% Atlanta Fed GDPNow model to the consensus of +.5%. As it turns out both were way off with the actual number being -.3%. The first negative GDP print since early 2022. As was widely expected, a massive surge in imports as companies attempted to front run the tariffs was the culprit. Slashing 5% from the quarterly GDP figure. Thanks to the BEA and WolfStreet for the chart.

Consumer Spending

Had another huge week with light vehicle sales jumping to 17.3 million units annualized in April. Once again front running looming tariffs was the culprit according to Wards Auto. Other notable economic reports for the week included Construction spending it fell .5% in March. Total non-farm payroll. AKA the jobs report handily beat expectations in April with a gain of 177,000 according to the BLS. Thanks to the Bureau of Labor Statistics and CalculatedRisk for the Chart.

Previous months were revised down by a combined 58,000. The unemployment rate was unchanged at 4.2%. Last but not least the spring real estate selling season is off to a slow start. Existing home sales fell 3.1% to a 16-year low in March to just 315,000 units. A 4.02 million annualized rate, inventory for sale jumped 8.1% to 1.33 million units, a little over 4 months supply.

Is the Coast Clear?

All in all, a very solid week of earnings and economic data. The sky definitely isn’t falling, though there are a few clouds. Trumps tariff messaging lacked polish, but he made some very good and long overdue points with our trading partners. The negative GDP report is likely to be revised away in the coming months. With 4 .25% rate cuts expected by the futures market this year. Perhaps real estate will find its footing. As affordability remains a real problem. While the media loves to lead with negative stories in the Trump 2.0 era. A recession became demonstrably less likely with the data released this week. Even though we got one negative GDP quarter and the official recession definition requires 2 consecutive negative quarters. Time will tell, it always does. But at this moment, I just don’t see it happening this year.

Last Week’s Post: Tariff Tantrum Fades From Memory

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Truth Social: Market Bull

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn