The major averages marked another positive week at the close. With the DOW up 669 points or 1.62%, the NASDAQ advanced 264 points or 1.49%, while the S&P 500 added 77 points or 1.37%.

Tuesday’s seasonally adjusted retail sales data revealed a surprising 0.1% gain in August, while July’s figures were revised up by 1.1%. This contradicts the notion of a weak economy. Remarkably, retail sales continue to rise even as the prices of many goods. Especially durable goods and gasoline have been dropping all year. This indicates that consumers are purchasing significantly more items, particularly durable goods. As illustrated by the 3-month moving average of sales chart on Wolfstreet.com.

Fed Chair Jerome Powell surprised everyone this week by slashing rates by ½% on Wednesday. Despite no market or economic emergency in sight, though there may be a significant political one. Historically, this cut was highly unusual. As it marked the first non-unanimous decision by the Federal Open Market Committee (FOMC) in quite some time.

While recent economic data has been fairly solid. The Bureau of Labor Statistics revised away 818,000 jobs on August 21st. Casting additional doubt on the strength of the labor market. This remains the only significant economic question mark at this time. Despite this, recent data has shown robust consumer spending. With people showing a real willingness to use their credit cards and spend freely. Party like its 1999 baby. Did I ever just date myself…

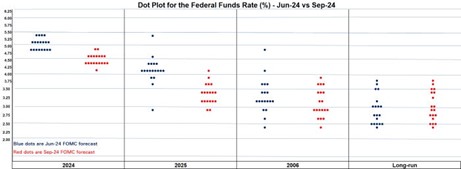

According to the latest FOMC Dot-Plot, another two ¼% cuts are expected before the end of the year. Followed by four ¼% cuts in 2025 and another two ¼% cuts in 2026. It seems interest rate analysts are once again indulging in irrational exuberance. Following another positive week but will see.”

Powell navigated the communications challenges of his press conference quite well. Presenting the ½% reduction as a one-off adjustment to right-size monetary policy. While aiming to lower inflation and shift distribution risk. The key for Powell, as Lindsay Rosner of Goldman Sachs noted. Was to convince investors that this was ‘a focused ½%, and not a fearful ½%.’ The week’s market gains, despite considerable volatility, support this view.

We used to hear a lot about pent-up investor demand for investments. With piles of cash in Money Market Funds sitting on the sidelines. This concept seems to have fallen out of fashion. Just like investing in Dot-Bomb stocks. There I go dating myself again. ☹ But it just might come back into vogue. According to the chart below from EPFR, Bloomberg, and the Federal Reserve. Money market assets have now reached an impressive $9 trillion. That has got to be burning a hole in somebody’s pocket. -right?”

Despite the positive news. A close analysis of the revised employment data, the Fed contracting the money supply over the last 2.5 years, and the inflation data. All strongly contradict the Fed’s official pandemic-era inflation narrative. Suggesting that inflation was caused by supply shortages. Due to various government pandemic isolation protocols. Also known as mandated shortages.

Historically, a contraction in the money supply means that the same level of economic activity and employment cannot be maintained at the same level of prices. Either economic activity and employment fall, or prices fall. Usually, economic activity and employment fall first, followed by prices, which then take profits down with them. This is why many pundits are predicting a recession or worse. So far, Main Street and Wall Street are winning this tug of war. Let’s hope that no political crisis disrupts what is currently a fairly solid set of market, economic, and business fundamentals as summer comes to a close following another positive week.