Despite finishing October on a rough note. The major averages wrapped up a usually difficult month mixed. The S&P 500 lost 53 points or .92%, the NASDAQ gained 185 points or 1.03%, while the DOW added 394 points or .94%. The performance of the major averages in an election year through October, however, is the best on record since 1936.

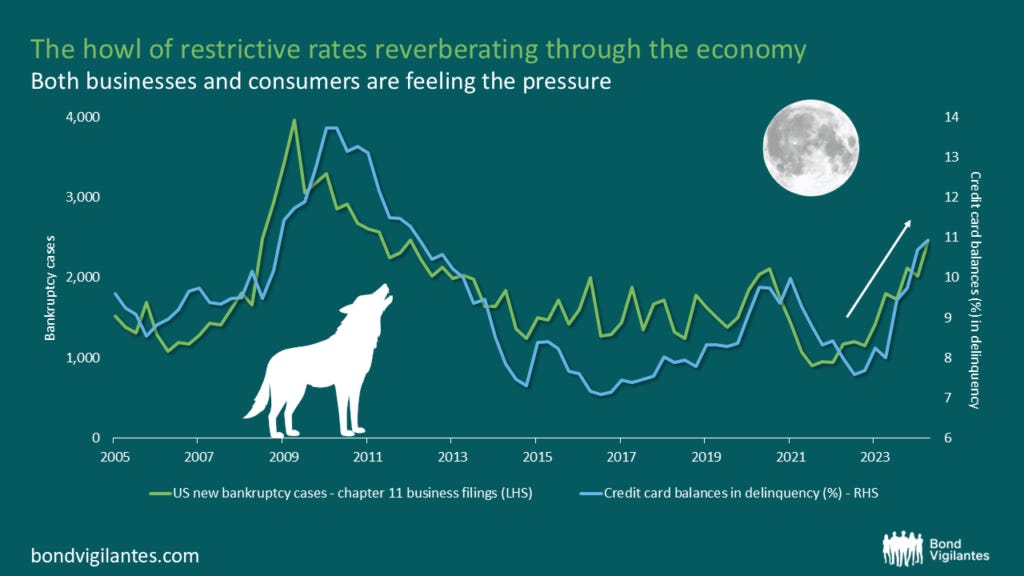

Despite the equity markets’ solid October performance. Bond markets came up short. Bloomberg’s global bond aggregate turned in its worst performance in a little over two years. Adding a jump in interest rates and disappointing October employment report. Gave the doom and gloom crowd plenty to talk about. Although it is true that monetary policy remains restrictive, and it has been for a while. It’s worth remembering that monetary policy works with a lag. The general rule of thumb is about 18-months. As a result, the effects are only now beginning to become evident. Something shown by the chart below compliments of the bondvigilantes. That shows rising credit stress, that like rising real estate for sale inventory. Although cause for concern, is not yet cause for alarm.

With Treasury yields, and as a result, mortgage rates. Continuing to grind higher, the 10-Year Note is knocking on the door for 4.3% a gain of some 65 basis points since the September lows. Just before the Fed surprised many, myself included with a 50 basis point cut. The argument for additional Fed rate cuts is solid.

Money, Money, Money

With the 3rd quarter S&P 500 earnings season progressing. A 12% plus profit margin for a second straight quarter is taking shape. If it holds, this will be the two best quarters for earnings since early 2022. Led by strong numbers for Real Estate, Information Technology, and Financials. Also of note, analysts expect net profit margins for the S&P 500 to exceed 12.0% for the next three quarters. 12.1% for Q4 2024, 12.6% for Q1 2025 and 13.1% for Q2 2025. Although a Republican election win is generally considered to be more favorable for the major averages. The only certainties in life are death and taxes. Thanks to FactSet for the chart.

A Soft Landing?

Of the significant economic reports released this week, the results were mixed. Advance 3rd Quarter GDP came in a little below expectations at 2.8%, a solid number, however. Pending home sales smashed predictions with a 7.4% gain on broad-based regional participation. PCE price data, the Fed’s favorite inflation metric. Was unchanged and remains fractionally above the Fed’s desired target of 2%. The BLS October Employment Report missed bigtime with just 12,000 new jobs created. The unemployment rate was unchanged at 4.1%. Hours worked remained the same, wages increased slightly. I wouldn’t put very much on this report however. As it is heavily impacted by two Florida hurricanes and a huge strike at Boeing.

That’s all for this week folks, I’ll see you again next Friday.

Best, Caleb

Last Week’s Post: 3rd Quarter Earnings Review

Follow me on Social Media

FaceBook: Caleb Lawrence RIA Inc Facebook

LinkedIn: Caleb Lawrence | LinkedIn