The major averages closed the week mixed with on again, off again tariffs driving uncertainty. Since Tuesday the S&P 500 gained 109 points or 1.89%, the NASDAQ picked up 377 points or 2.01%, while the DOA gained 667 points or 1.6%.

With lawfare driving uncertainty with respect to tariffs and most everything else Trump related. It’s difficult to get fix almost anything. As analysts, investors both foreign and domestic, business owners and our trading partners try to make sense of it all.

Foreign Investors

Are critical to the efficient functioning of our capital markets, financing both government debt and deficits through direct foreign investment and the purchase of Uncle Sams best paper, aka Treasuries. One of the post Liberation Day narratives pushed by the lamestream media was that the tariffs would ignite a trade way, drive away foreign investors. Triggering a currency crash and massive recession. The TIC report or Treasury International Capital report measures and records foreign direct investment and Treasury purchase with a 2-month lag. So we are still waiting for April’s release. February and March both came in very strong. Most of the Treasury auctions have also shown solid demand. Suggesting that the April TIC Report should be solid as well. In turn destroying another lamestream media TDS driven narrative.

But, Interest Rates

The latest FOMC Notes for May show a Fed in no hurry to change interest rates. As the Fed adopts a wait and see approach, as it to has to cope with the uncertainty, much of it driven by record setting lawfare against Trump 2.0. To quote; “FOMC participants continued to view the current monetary policy as moderately restrictive and the economy as growing at a solid pace, with labor market conditions broadly balanced and inflation somewhat elevated. However, they viewed uncertainty as high, with intensified downside risks to employment and economic growth, and upside risks to inflation”. This pushed rate cut expectations in 2025 down to just one ¼ point cut in December. Though multiple cuts are still expected in 2026. Take that with a grain of salt. As our overly optimistic analyst friends tend to get carried away with their rate cut predictions.

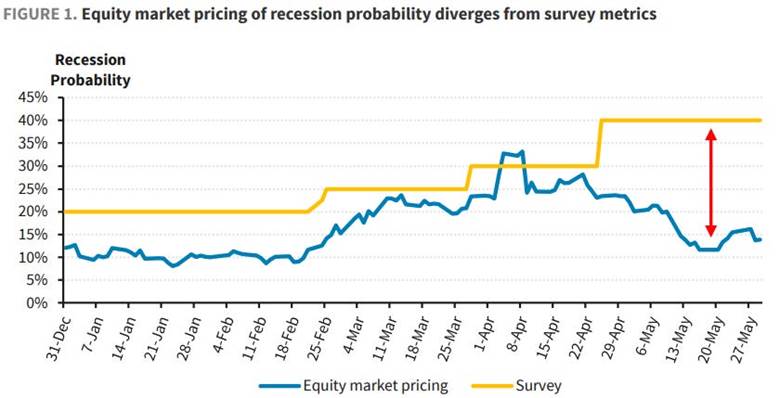

About That Recession

The hard economic data says “no recession” anytime soon. The soft or survey data is thinking about as the lamestream media continues it’s best efforts to scare the beejesus out of everyone. So far with little success. Looking at the equity markets and their estimation of a recession has decreased fairly steadily since liberation day. As the chart below shows, Compliments of Barclays PLC.

The second revision to 1st quarter GDP remained negative but improved to -.2% per the BEA or Bureau of Economic Analysis. Uncertainty caused a notable .6% downward revision to PCE to 1.2% growth. Prices were largely unchanged, the PCE Core Rate slipped .1% to 3.4%. Moving to the BEA Personal Income and Outlays report for April. We have solid personal income up .8%, same as disposable personal income. Personal consumption expenditures, aka consumer spending increased .2%. Uncertainty strikes again as consumers chose to save more pushing the savings rate to 4.9%. Despite a few glitches the economic data continues in its good, but not great muddle along fashion popular of late.

Last Week’s Post: MSM Doom and Gloom

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn

Leave a Reply

You must be logged in to post a comment.