With the irrational exuberance of the post-election market euphoria wearing off. The major averages recorded a rough first full week to start the year. The DOW lost 763 points or 1.79%, the NASDAQ fell 434 points or 2.22% while the S&P 500 gave up 112 points or 1.89%.

Equity Risk Premium

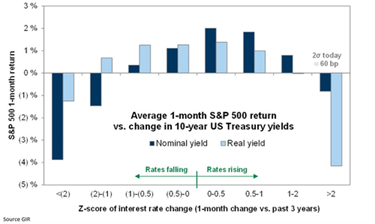

The recent spike in interest rates, despite 1% of cuts by the Federal Reserve to close 2024. Driven by the normalization of the yield curve. Following a long period of inversion, though no recession. Left the market Bulls wringing their hands and muttering about animal spirits and irrational exuberance. From a historical perspective equities typically struggle when interest rates rise by 2 standard deviations in a given month. Which in today’s terms is ~60bps, aka .6%. As the chart below shows, compliments of GIR.

With the 10-year Treasury testing 4.7% the pressure on equities markets is high and rising. Market strategists like to point to the equity risk premium. Or the S&P 500 earnings yield over the current 10-year Treasury rate. When it drops, or falls below zero, stocks are expensive. To quote Alan Greenspan, former Federal Reserve Chairman, love him or hate him. At present this measure now says that stocks are their most expensive since 2002. Coincidentally at exactly the level on Dec. 5, 1996, that prompted Greenspan to sound his “irrational exuberance” warning. A few noteworthy items relevant to our equity risk premium discussion. The problem here stems from an unusual spike in interest rates. As the curve normalized after a lengthy period of inversion. This is good news from an economic perspective. For the most part the economic data remains positive overall. Historically, the most common driver of significant market losses are recessions. Something we saw during the severe market declines in 2008 and, to a lesser extent in 2020. The Dot-Com market decline led to a recession a year later in 2001. Having said all that the chart below, compliments of Bloomberg, is worth noting.

Animal Spirits, Can President Trump Deliver?

Some six decades before Greenspan, John Maynard Keynes the famous economist and father of the Keynesian school of economic thought. Proffered the concept of animal spirits in his General Theory of Employment, Interest, and Money, in 1936. To quote Keynes: “A large proportion of our positive activities depend on spontaneous optimism. Rather than on a mathematical expectation. Most, probably, of our decisions to do something positive. Can only be taken as a result of animal spirits. A spontaneous urge to action rather than inaction. Not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities”. Something to keep in mind. The next time an economist claims that we all act out of rational self-interest, but I digress.

Historically Republican administrations are usually good for stocks. Stocks require a certain amount of animal spirits, efficient market theory notwithstanding. During the Trump political era, 2016 to the present. Two periods of “animal spirits” standout. Late 2016/early 2017 and the present, currently being tested. It’s hard to explain current asset prices without invoking an abstract concept like “animal spirits”. Trump is the best explanation for their resurgence. With stocks riding a wave of potent optimism that Trump 2.0 will be good for the market. The question is, will it last? Thanks to Bloomberg for the chart.

Will Strong 4th Quarter Earnings Support Valuations?

The latest data from FactSet indicates that the S&P 500 will record the highest earnings growth in 3-years. With the 4th quarter expected to show final earnings growth of 17.3%. This comes from the current estimated growth of 11.9% and the historical earnings beat rate of 5.4%. With 22 companies having reported earnings to date, 77% have beaten the estimate so far. While it remains early to be sure. Realistic earnings growth estimates for the 4th quarter run from 11.9%, the official estimate at present. To as high as 19% based on recent S&P 500 performance. So, with a little luck, solid earnings. A few more interest rate cuts in 2025. Animal spirits will be driven by a strong start to Trump 2.0 helping to support current valuations and decent 2025 investment returns.

Caleb

Last Week’s Post: Political Infighting, Can’t We All Just Get Along?

Follow me on Social Media

FaceBook: Caleb Lawrence RIA Inc Facebook

LinkedIn: Caleb Lawrence | LinkedIn