Another good week for the major averages on positive data. While the bromance between Musk and Trump seemed to hit the skids this week. I had to wonder. Was this another of President Trumps infamous trolls of the lamestream media?

Since Monday the S&P 500 gained 88 points or 1.49%, the NASDAQ advanced 416 points or 2.18%, while the Dow added 493 points or 1.17%.

60-Days And Counting

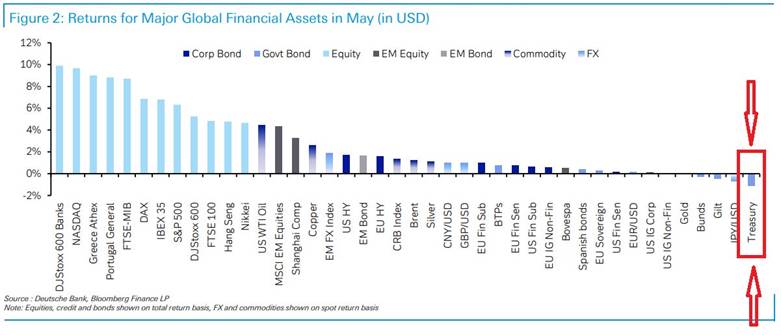

Since Liberation Day, despite endless doom and gloom from the mainstream media. May was another solid month for most investments. The S&P 500 added 6.3% for the month its best showing in 18-months. Credit spreads tightened meaningfully indicating that the credit markets returned to normal after all the turmoil. Treasuries and long dated corporate bonds still struggle. I would expect them to settle down soon enough. Most likely after Trumps “Big Beautiful Bill” passes and the credit markets get some clarity on taxes, deficits and the federal budget. Moody’s credit rating downgrade was largely symbolic. The chart below compliments of Deutsche Bank lays out the score for May.

Lawfare Rages

Activist judges continue to block President Trumps agenda at every turn. After the USCIT or US Court of International Trade struck down the latest round of tariffs this week. Only to be almost immediately overturned on appeal following a Trump administration motion. Despite all this the outlook for tariffs and the economy remains largely unchanged. The effective tariff rate still looks to be running about 13%. The consensus for a sharp slowdown in May employment growth per the chart from Apollo below that estimated just 64k new jobs.

Was instead blown out by today’s non-farm payrolls report. The Bureau of Labor Statistics reported a slightly above expectations figure of 139,000 new jobs. More than double Apollos dismal estimate. Average hours were unchanged at 34.3. Average hourly earnings jumped .4%, handily beating expectations. The unemployment rate remained unchanged at 4.2%. The only real negative was a downward revision to previous months of 95,000. A good, but not great employment report following the recent trend.

Mirror, Mirror On The Wall

Does this mean no recession? The only two things in life that are guaranteed are death and taxes. Looking at the latest JOLT or Job Opening and Labor Turnover data . Shows that the job vacancy rate remains above the unemployment rate. It is very hard if not impossible to generate a recession under these conditions. If history is any guide. Thanks to BCO research for the chart below.

Last Week’s Post: Driving Uncertainty

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn

Leave a Reply

You must be logged in to post a comment.