After opening the week with huge gains. The Capital Markets drifted into Friday, posting large declines. Finishing the week decidedly in the red. Erasing much of post correction gains. Since Monday the S&P 500 is down 87 points or 1.54%, the NASDAQ lost 461 points or 2.59% while the DOW slipped 401 points or .96%. The markets don’t like uncertainty. After today’s performance, they don’t seem to like Liberation Day either.

Who Likes Tariffs

The rubber is about to meet the road as they saying goes. Liberation Day or April 2nd will see the implementation of a “reciprocal tariff” framework. Equal to other countries’ tariff, VAT, and non-tariff barriers treatment of US imports. While a 25% tariff will be applied to foreign autos as well. Like the tariffs before this. A number of last-minute deals have already been worked out. India in particular comes to mind. These should serve to blunt the negative economic impacts, as has been seen in the past. Auto tariffs will hit the following manufacturers particularly hard. Thanks to Global Data and Bloomberg for the chart.

Many an economist and free trade proponent will decry tariffs. Pointing out that they stifle trade, add inflation and curb global economic growth. It is hard to argue against these points. They also provide significant economic benefits as well. Cutting trade deficits, re-shoring employment, increasing the tax base and spurring domestic development. Then there are the national security benefits. Outsourcing a country’s manufacturing base to the point that it degrades national security. While fraying the fabric of society is neither a desirable nor sustainable strategy.

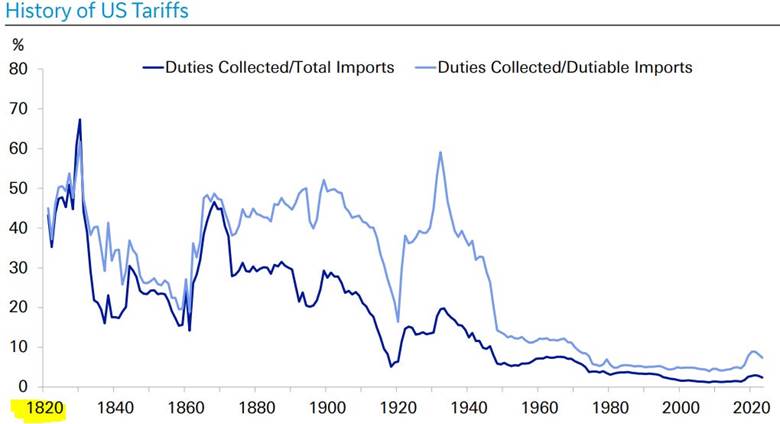

All things considered. It is not surprising that the US is turning to tariffs if you look at the full sweep of history. America has a long history of tariffs, which played a key role in the early industrialization of the nation. Of note with the chart below, tariffs declined sharply in the early 1900’s before they rebounded. Remember 1913? That was the year America introduced the income tax following implementation of the Revenue Act of 1913. Taxes started at 1% and went as high as 6%, simpler times.

Will The Economy Survive

The most significant economic report this week was the Chicago Fed National Activity Index (CFNAI). It gained .18 in February on a broad based advance. The 3-month MA increased to .15. This series covers about 85% of economic activity and -.7 for the 3 month MA is generally regarded as indicating a recession. So far so good, let’s check in with the Federal Open Market Committee. To see where they think the economy is headed.

The degree of disagreement on the committee is remarkable. With one FOMC member saying that in 2026, the Fed funds rate will be almost 4%. Other FOMC members saying that they think interest rates in 2026 will be just above 2.5%. The dot plot also shows that there is debate. About where the Fed funds rate will be in the long run, with a range between 2.5% and 4%. Perhaps most importantly, none of the FOMC members are predicting. A sharp decline in the Fed funds rate to zero. Telling the market that nobody on the FOMC is expecting a recession. Thanks to Apollo Academy for the chart.

Did The Capital Markets Bounce

Despite the recent “official correction” of 10% seen with the major averages. It would appear that a solid technical bounce off the bottom has occurred. Thanks to PaulsenPerspectives for the chart.

The upshot is that although the US equity market volatility. Will undoubtedly make many CEOs nervous, yours truly and many an investor. It does not have the hallmarks of prior sell-offs. That were actually associated with a serious dip in corporate and economic activity. Consider that projected earnings remain strong, credit is plentiful, and private capital backstops the market. And although economic uncertainty is very high, it is a ‘controllable’ factor for the economy – i.e. It is controlled by government policymakers (predominantly the President). That contrasts with ‘uncontrollable’ factors such as the subprime loan crisis or contagion over fears about sovereign debt.

Earnings Finished Strong

On the subject of earnings, the final 4th quarter GDP report is out, +2.4%, including the corporate earnings numbers. As I have mentioned previously, they are solid numbers indeed and well above expectations. Profits advanced an impressive 204.8 billion in the 4th quarter. A dramatic improvement over the 15 billion profit decline recorded in the 3rd quarter of 2024. For all of 2024 profits totaled 3.83 trillion Dollars with inventory valuation and capital consumption adjustments. A gain of 281.3 billion over 2023 or 7.93 percent. Hard to argue with numbers like that. Thanks to the Bureau of Economic Analysis for the data.

Also, of note 4th quarter S&P 500 earnings finished with record high. Earnings Per Share (EPS) and Revenue Per Share (RPS) and a 12.8% profit margin. Per the chart below compliments of LSEG DataStream, Yardeni Research and Standard and Poors.

Rejection of Liberation Day not withstanding. I expect the volatility, bumpy market and economic ride to continue through the second quarter. After that things should improve noticeably. FactSet research released a report late today estimating a 21% gain for the S&P 500 over the next 12 months.

Please hit the like and share buttons. Have a great weekend, I’ll be back next Friday.

Last Week’s Post: Tariff Tantrum Over?

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Truth Social: Market Bull

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn