This week was full of surprises as well. Trump’s announcement this afternoon of 25% tariffs on Mexico and Canada spooked the markets. Sending them into the close mixed. Since Monday the S&P 500 lost 60 points or .98%, the NASDAQ slipped 327 points or 1.64%, while the DOW gained 121 points or .27%.

The Economy Was Also Full Of Surprises This Week

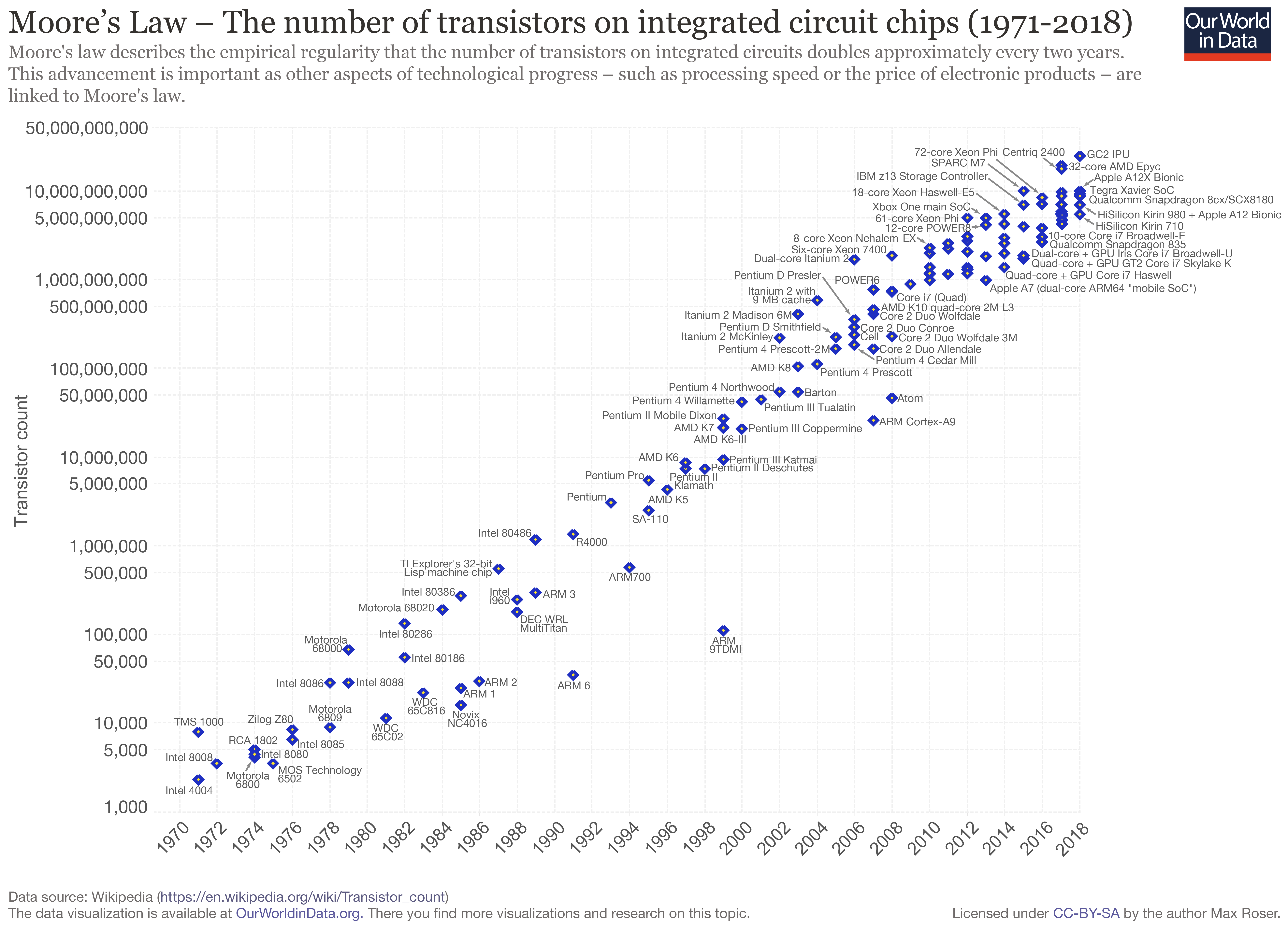

4th quarter GDP estimates took a real hit falling to just 2.3%. After businesses piled up orders ahead of the expected tariffs. Skewing the trade data. While ongoing troubles over at Boeing negatively impacted the volatile transportation component of the Durable Goods Orders report. Disappointing to be sure, but one month does not make a trend. Other surprises this week included the debut of Chinese AI DeepSeek. A competitor for American AI systems reported to cost a fraction of the price of rivals like ChatGPT. It is too early to tell for sure if the hype is real. But the Chinese do have a real knack for making things cheaper than anyone else. I’ll also not that it is the historical experience with technology. For it to get faster and cheaper exponentially over time, remember Moore’s Law? Transformative technological change creates winners and losers, and it stands to reason that the consumer of AI technologies. Individuals and firms outside the technology industry. Will prove the main winners from the release of a high-performing open-source model. Thanks to Our World in Data for the chart.

The Dominant Themes In 2025

Will be inflation and interest rates, with tariffs on the side. The Fed’s hawkish pause on interest rates this week. Following the latest FOMC meeting on the subject. Isn’t likely to sit well with President Trump. Expectations for further cuts this year are pretty nominal at this point. With traders expecting just 1 or 2 .25% cuts by year end. With work remaining on normalizing the yield curve. Either long rates have to rise further, or short rates need to decline. Ala rate cuts, or perhaps a bit of both. Looking at inflation and the world looks increasingly deflationary. Global industrial production capacity remains anemic. This should put considerable downward pressure on prices. Trump’s promises to “Drill Bay, Drill” is likely to ramp up energy production putting further downward pressure on inflation. Deregulation and a dramatic tightening of immigration policy. Already underway from coast to coast. Will likely prove mixed bag with respect to inflation. Tariffs on the other should prove inflationary, but not as much as most people think. It is not a linear equation. A 25% tariff on Mexico and Canada for example does not equate to a 25% increase in prices, aka inflation. For the following reasons. They are not our only trading partners. Consumers purchase goods and services from a variety of sources. Lastly domestically produced goods and services, the Lions share, aren’t tariffed.

Caleb

Last Week’s Post: The Winds Of Change

Follow me on Social Media

FaceBook: Caleb Lawrence RIA Inc Facebook

LinkedIn: Caleb Lawrence | LinkedIn