Despite the major averages finishing the week with significant gains there’s more work to be done. They have only managed to recover about half of the Liberation Day carnage so far. Leaving more progress to be made. Since Monday the S&P 500 has gained 339 points or 6.75%; the NASDAQ is up 1,136 points or 7.29%: while the DOW added 1,898 points or 4.95%. The recent volatility that sent the VIX index to a 5-year high north of 46. Also sent market valuations to about fair value, if only briefly. Despite what was a deteriorating outlook for earnings growth. Thanks to Bloomberg for the chart.

There’s more, S&P 500 earnings estimates are picking up and now exceed 10%. This despite continued recession stories out of the MSM who also continue to push the inflation narrative as well. Neither is supported by the incoming data. MSM true to form, never let the facts get in the way of a good narrative.

Do You Feel Like A Yo-Yo?

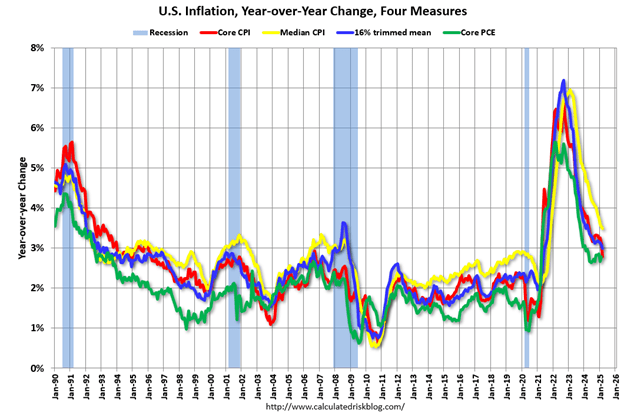

While asset prices have gone all over the map in the post Liberation Day period. Oil fell sharply beginning in April and is now down almost 14%. Should this price hold through the end of the month. It will add another significant downward leg to inflation in April. Building on the declines recorded by the CPI for March down .1% for the month and up just 2.4% from a year ago. The PPI fell .1% for the month as the annualized rate declined to 3.3%. All the inflation data came in below expectations. Despite the naysayers, inflation continues to trend lower. Thanks to CalculatedRisk for the chart.

The 6-Sigma miss in consumer credit was also good for numerous MSM headlines screaming about a recession. Consumer credit fell .81 billion, a dramatic miss from the expected gain of 15 billion, while previous months were revised lower. A disappointing report to be sure. The MSM claiming one month’s data is proof of a recession inbound is irresponsible at best. More accurately sensationalistic narrative with an eye to selling advertising copy.

But Wait, There’s More, No Less Tariffs.

Tariffs and there on again off again nature this week. Along with a full blown in your face tit-for tat with China that saw trade essentially halted as tariffs on both sides very quickly escalated over 100%. Served to spook the markets, and just about everyone else this week. Despite the 90 Day pause afforded by the Trump administration. I believe that tariffs are important and that the trading field is seriously skewed against the US. The 10% tariff rate flip flopping this week strongly suggests that the Trump Team didn’t think the tariff process through as well as they could have. Something demonstrated by the disjointed messaging this week. While economic growth or GDP estimates remain positive this year. The recession probability has increased to 45%.

Who’s on 1st? Who’s on 2nd? Who’s on 3rd? -who knows.

Uncertainty is extremely hard on businesses and consumers alike as it makes an already tough job, trying to predict the future, essentially impossible. Which in turn crimps investment and spending plans. The longer this continues the broader and more painful the economic effects will become. Which is of course much of the impetus for the rising recession odds.

Trumps signature negotiation style is infamously chaotic. At the same time it is also very successful. Certainly the world has been put on notice that the status quo will not continue. Change, with a capital “C” is on the table. Change for a lot of people is synonymous with fear. Can the current administration restructure the global security and trading paradigm without turning the world on its head? Time will tell. It always does. The process would be a lot easier if the obviously biased MSM wasn’t trying to scare everyone to death with its blatant hatred of Trump. While trying to prop up the morally, ethically and spiritually bankrupt Democrats.

Last Week’s Post: Tariff Terrorists Strike

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Truth Social: Market Bull

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn

Leave a Reply

You must be logged in to post a comment.