A rough week for stocks sends the major averages into the close with meaningful losses. As the markets chalk up their first down week since October 7, when they finished fractionally lower. Since last Friday’s close the S&P 500 has lost 111 points or 1.62%; the NASDAQ fell 720 points or 3.04%; while the Dow slipped 676 points or 1.42%

The Gift That Keeps On Giving

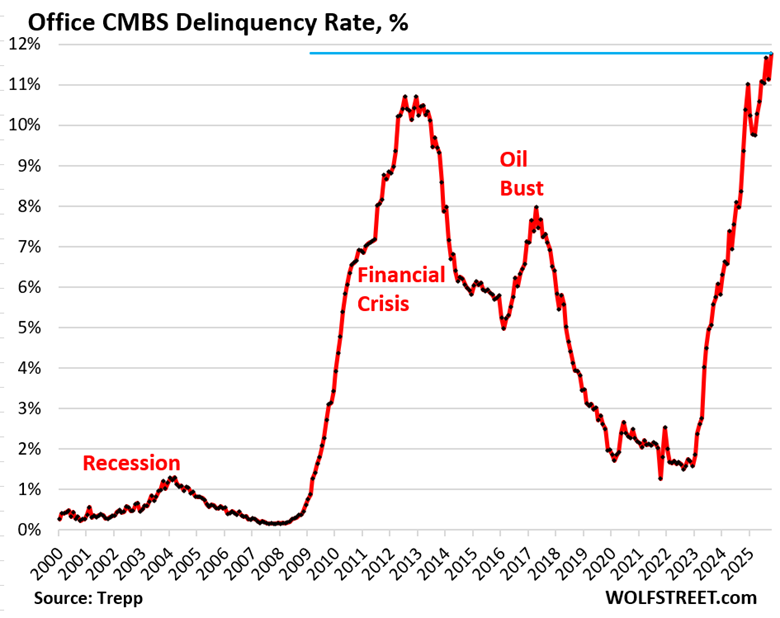

Covid-19 changed the world, and many would argue. Not for the better. One of the hallmarks of significant events such as this is the law of unintended consequences. Covid radically altered the concept of work. Particularly white-collar office work. Something that is showing up in record office vacancy, and now mortgage delinquency rates. The latest data from Trepp. Shows that the CMBS or commercial mortgage backed securities used to finance large office properties. Have seen their delinquency rates blow out to a record 11.8% in October, surpassing the previous record set during the Great Financial Crisis or GFC back in 2012. Thanks to Trepp and Wolfstreet for the chart.

Housing Affordability

Another unintended victim of the Covid fiasco. While slightly off its record 2022 high, remains patently unaffordable based on the price to income ratio. It is harder to calculate than the usual affordability metrics quoted. Due to the significant lags associated with income data. Nonetheless it is one of the better metrics of home affordability. Thanks to CalculatedRisk for the chart.

Using data from the Case-Shiller house price index and the 2024 Census Bureau nominal median household income series. Estimated 4% income growth for 2025. We find that while the price to income ratio is slightly off its recent record high. Incomes still need to rise significantly from here.

Show Me The Money

With the 3rd quarter earnings reporting season for the S&P 500 companies 91% complete. Results are well ahead of expectations according to FactSet Research. Surprising as analysts are an unusually optimistic bunch as a general rule. A fourth consecutive quarter of double digit earnings growth is tracking 13.1%. Far higher than the anemic 8% expected at the end of September. Revenues are also running strong up 8.3%, a 3-year high. So much for the doom and gloom crowd and their dire predictions earlier this year. Wrong on GDP, wrong on inflation, wrong on earnings, and wrong on the markets.

Have a great weekend everyone! See you next Friday.

Last Week’s Post: The Shutdown Continues

Follow me on Social Media

Comments

One response to “Meaningful Losses”

[…] Last Week’s Post: Meaningful Losses […]