The major averages put the tariff tantrum to rest. With 4 consecutive gains this week. As the major averages closed with impressive gains. Since Monday the S&P 500 increased 242 points or 4.58%, the NASDAQ jumped 1,097 points or 6.74% while the DOW gained 971 points or 2.48%.

This week’s gains have all but erased the tariff tantrum losses. While pushing the volatility index or VIX down to a 23-day low of 24.84. Only slightly higher than the 21 and change pre tantrum low seen in the fear index, as it is often called.

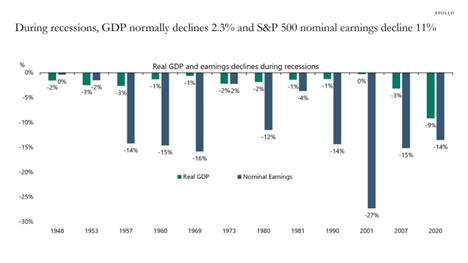

A Recession Is Coming?

There’s no shortage of pundits calling for a recession, negative earnings and worse. Following the much-criticized Liberation Day tariff rollout. To be sure the messaging left a lot to be desired. From a historical perspective in the post WW 2 period. GDP has declined 2.3% on average, while earnings have fallen 11% on average during a recession. Per the chart below compliments of Apollo Academy.

The media loves to criticize all things Trump. But a hard look at the data shows Q-1 earnings prospects improving. While monetary and economic conditions remain accommodative and fairly positive respectively. Despite calls for sharply lower interest rates and criticism of Fed Chairman Powell. The reality being that most of the current problems with respect to the economy, inflation and monetary policy stem from the Biden administration. Just don’t tell the mainstream media that.

Is The Cat Out Of The Bag?

Despite the events of the last few weeks. Economic data has remained fairly positive, though Thursday’s significant jump in Durable Goods Orders should be taken with a grain of salt. It is hard to argue for an imminent recession at this time. Despite still negative Atlanta Fed GDPNow estimates. The consensus is less than 1%, but still positive. Moving to earnings, the latest data for the 1st quarter is expected to trail the solid 4th quarter numbers. Things are looking up, as Factset Research reports that Q-1 earnings growth is tracking just over 10%. While revenue growth is pushing 4.6%. Less than Q-4 2024 to be sure, but solid numbers just the same with 36% of companies reporting so far. Results are being led by the Health Care and IT sectors. Thanks to Factset Research for the chart.

Last Week’s Post: Extreme Markets

Follow me on Social Media

X: Caleb Lawrence (@CalebRIAInc) / X

Truth Social: Market Bull

Substack: @themarketbull

LinkedIn: Caleb Lawrence | LinkedIn

Leave a Reply

You must be logged in to post a comment.